I’m particularly sensitive to this one because of the outrageous fees I’ve seen in the church plan 403(b) world.

401(k)s and standard 403(b)s certainly aren’t immune either, but church plans can be some of the worst offenders.

This is a shame considering they are for, you know, CHURCHES.

But have no fear, they will serenade you with “Just as I Am” while you’re on hold.

I could go on.

Being held hostage by these fees because you don’t have a choice is frustrating.

To understand your plan’s fees, ask your plan’s administrator (Executive Pastor, HR, Elder Board, Finance Deacon, etc.).

Be sure to ask them for all plan associated fees which can include recordkeeping fees, third party-administrator fees, advisory fees, and managed account fees.

They can reach out to the plan provider if they aren’t sure.

Another thing to keep in mind is the default plan investment option, known officially as the QDIA.

This QDIA is another way fees can get snuck into the mix when the plan provider’s proprietary options are used.

The provider knows that most people use this option.

So, they funnel people into their fund that is more expensive for you but more profitable for them.

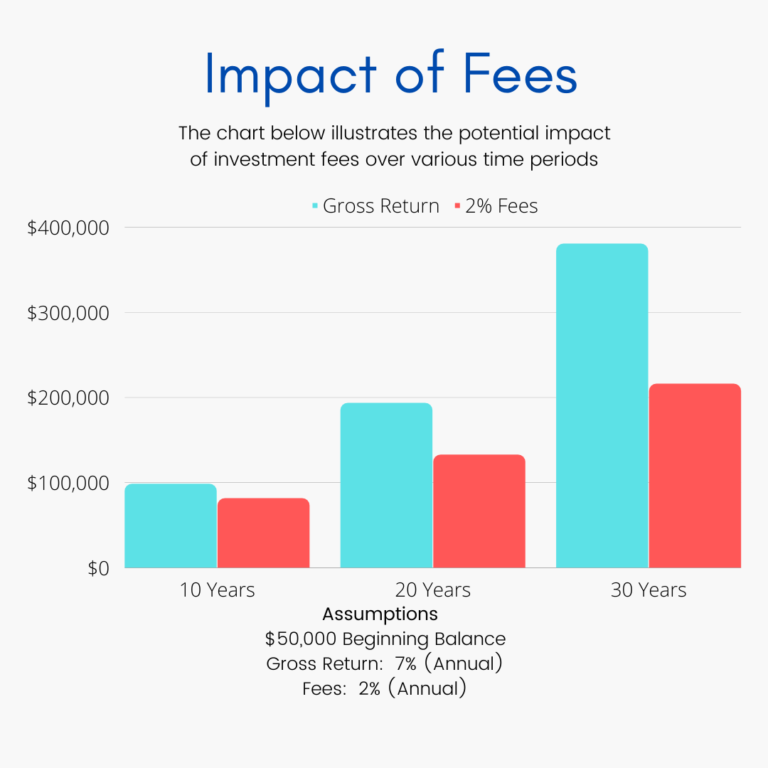

All these fees can be choking out your returns without you even knowing it.

Unfortunately, small employer plans can be easy targets for these fees, especially church plans.

What can be done about this?