Biblically Responsible Funds are actively managed funds.

Therefore, investors that have adopted a low-cost, passive index-fund investment approach will likely find themselves at odds with the active investment approach of BRI funds.

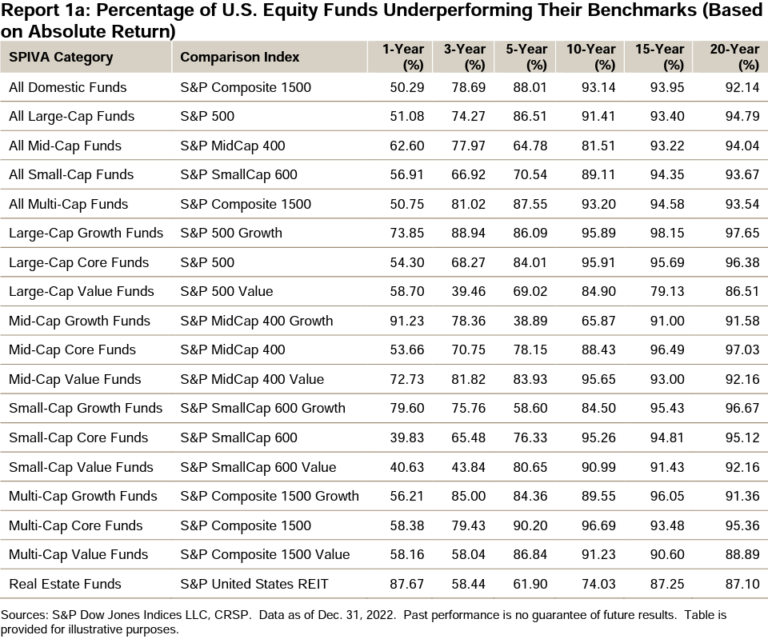

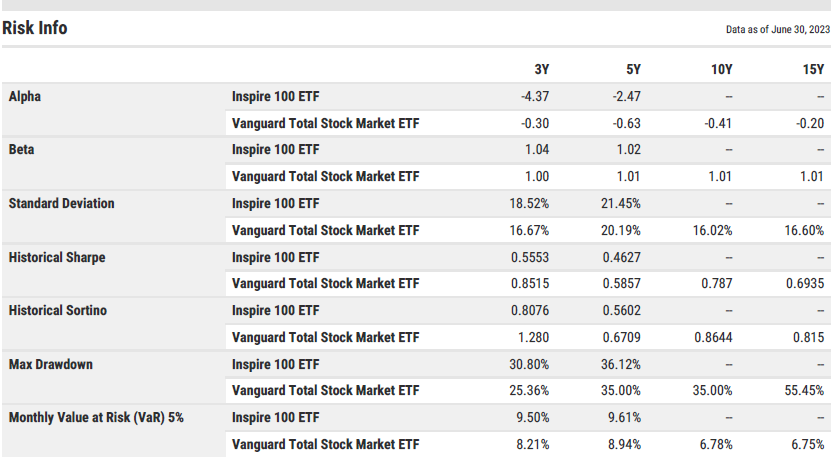

The performance challenges of active management are well documented.

According to the annual SPIVA study (chart below), over 90% of all actively managed funds underperform their benchmarks over the long-term.

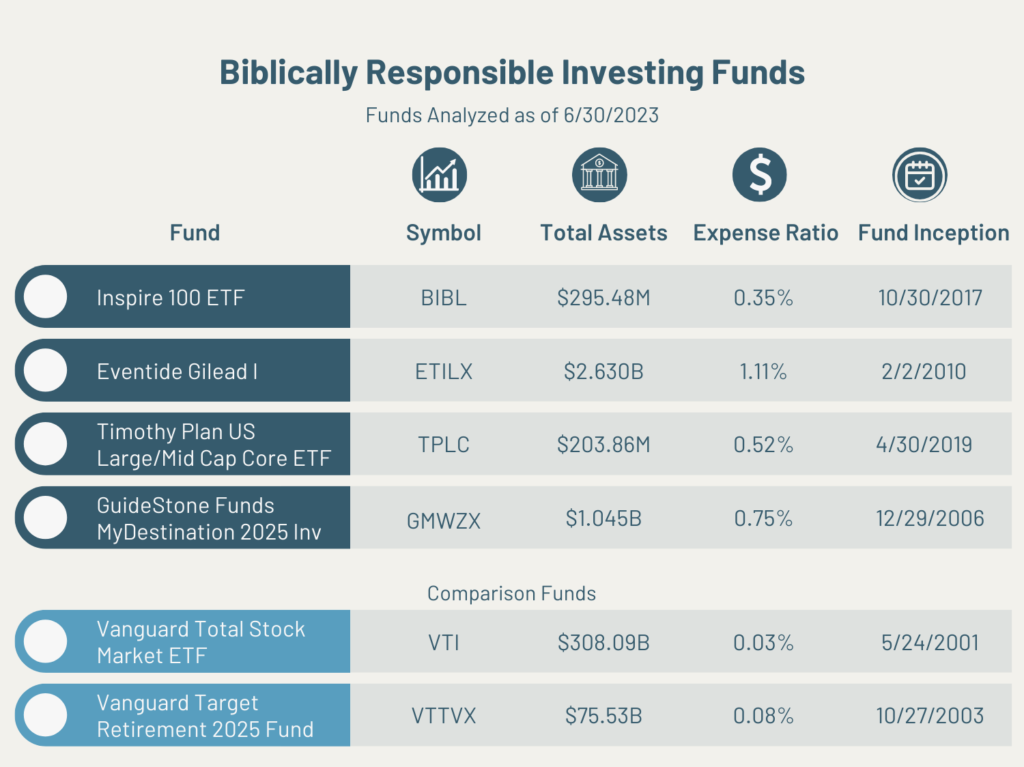

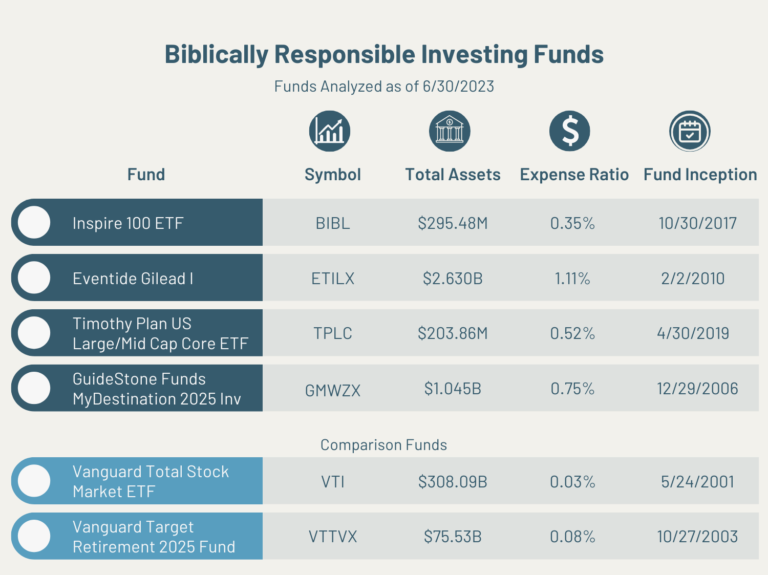

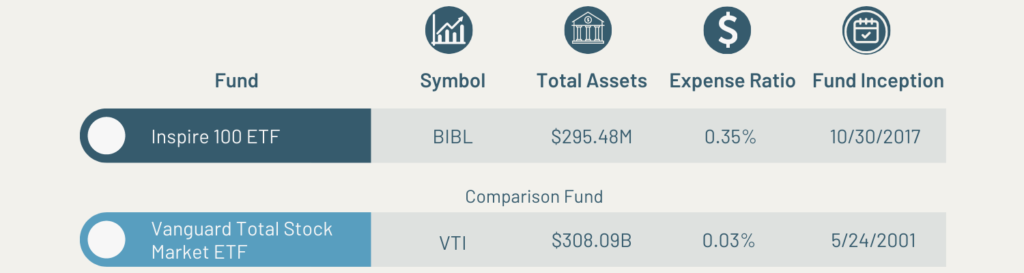

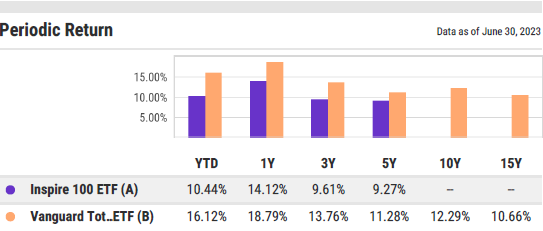

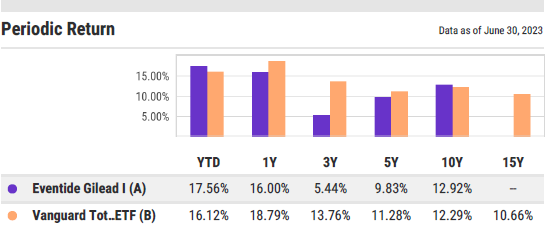

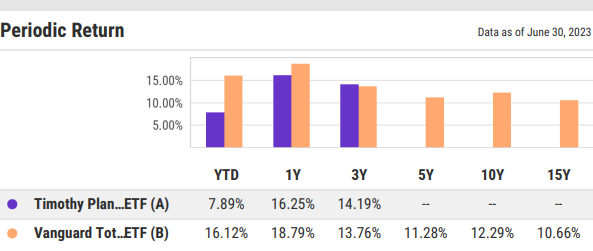

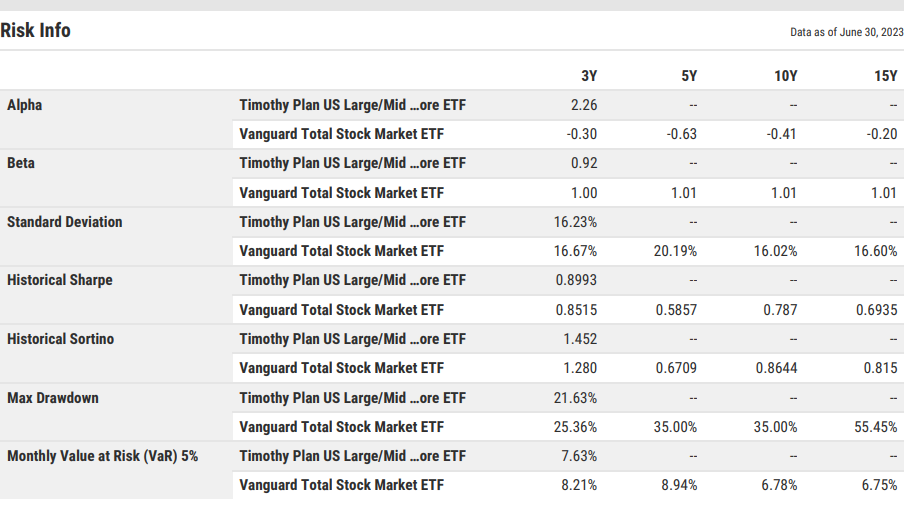

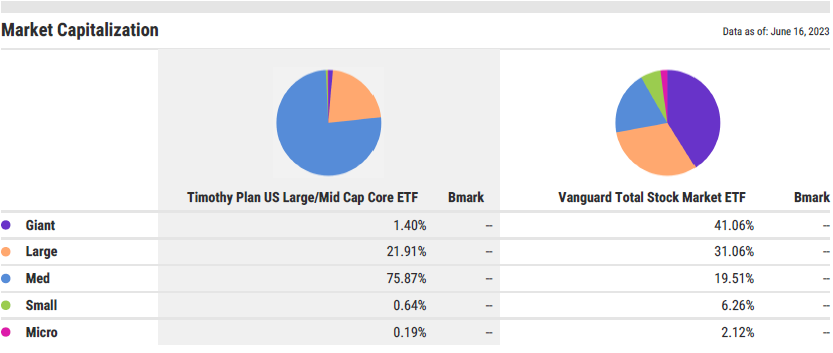

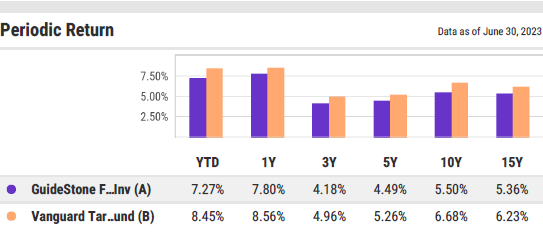

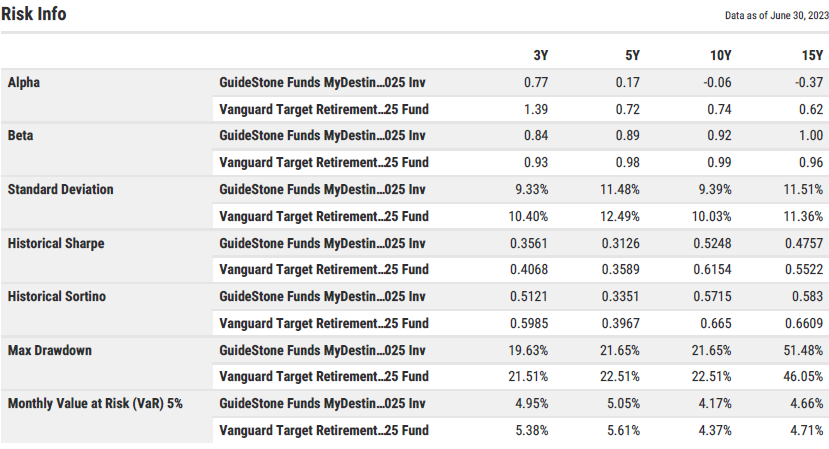

After analyzing four popular BRI funds, they are not an exception to this rule.

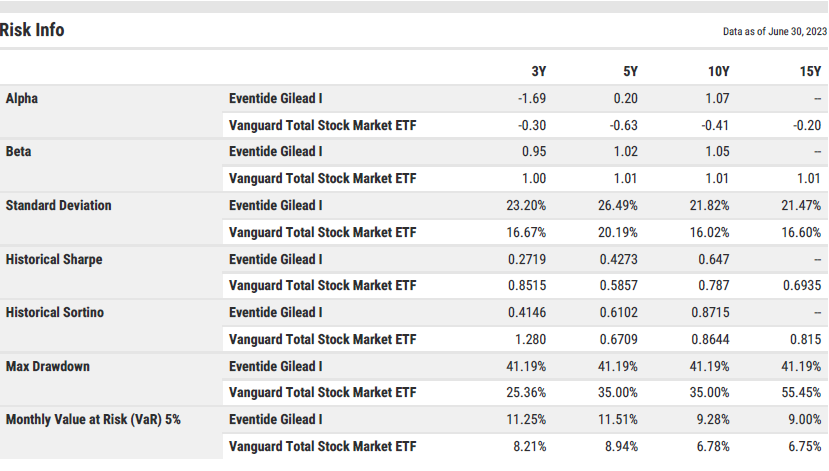

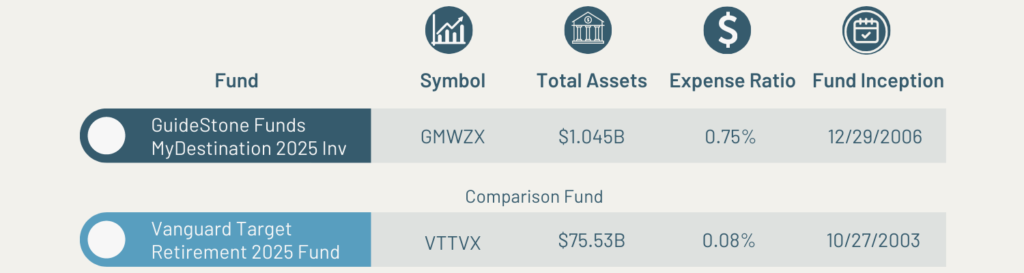

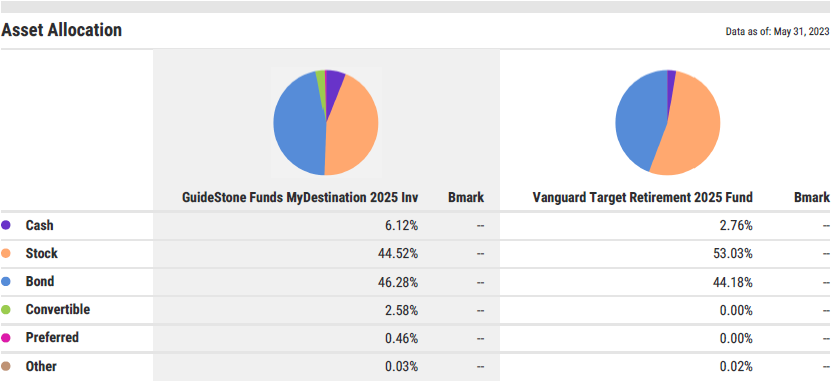

Each fund analyzed has experienced significant periods of underperformance when compared to a U.S. Total Stock Market Index Fund (for the three U.S. stock funds) or a passively managed target date index fund (for the target date fund analysis).

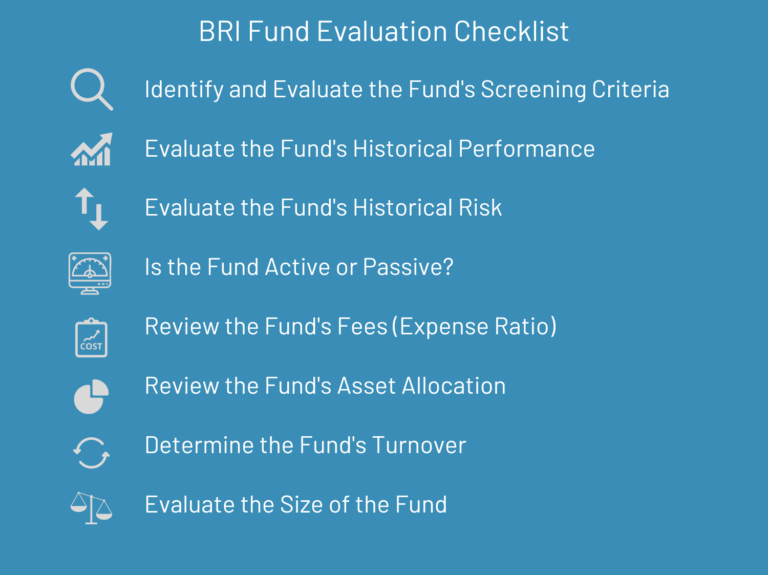

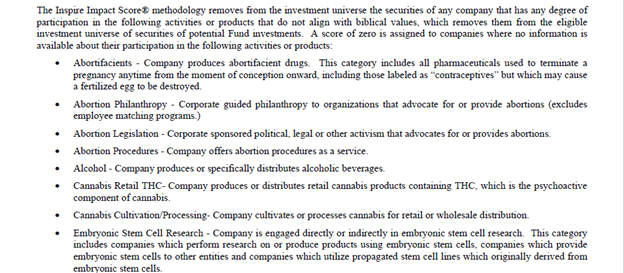

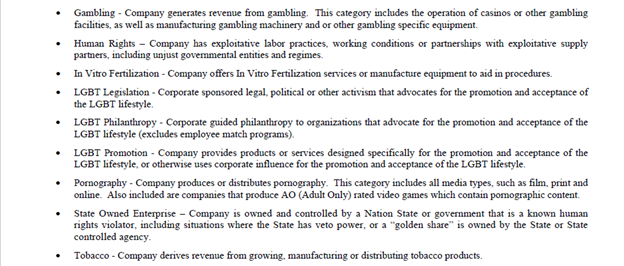

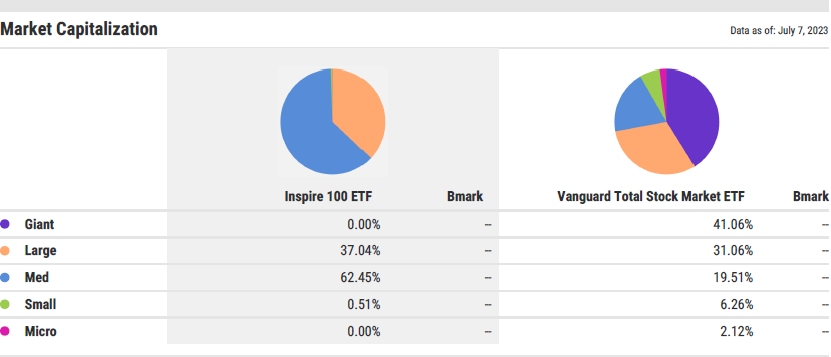

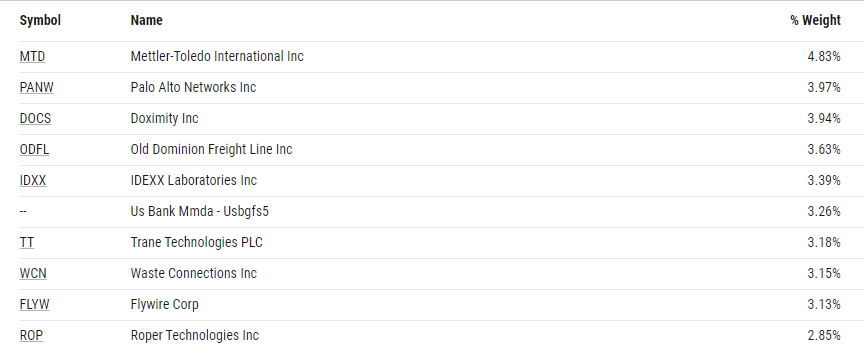

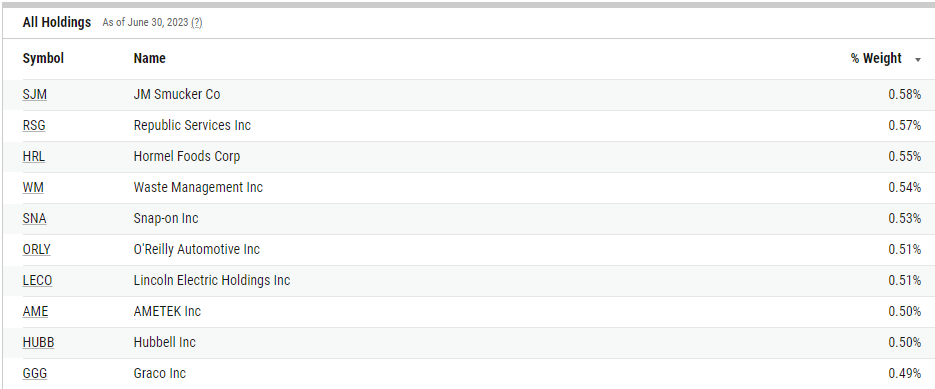

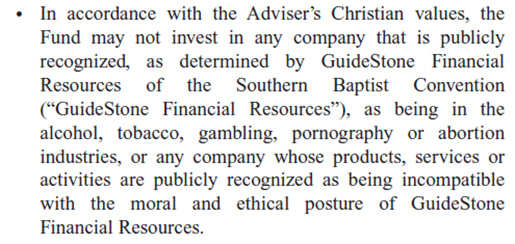

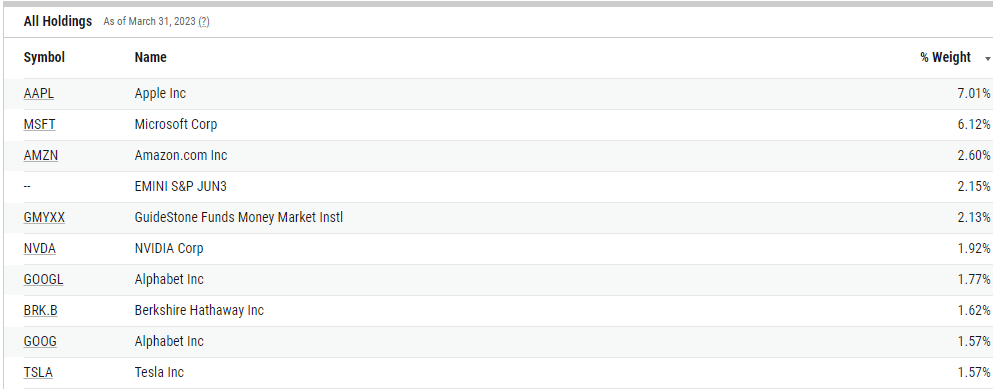

In addition to the performance challenges, ensuring that an investor’s values are represented within the fund’s securities is just as difficult because the security selection decision is inherently subjective.

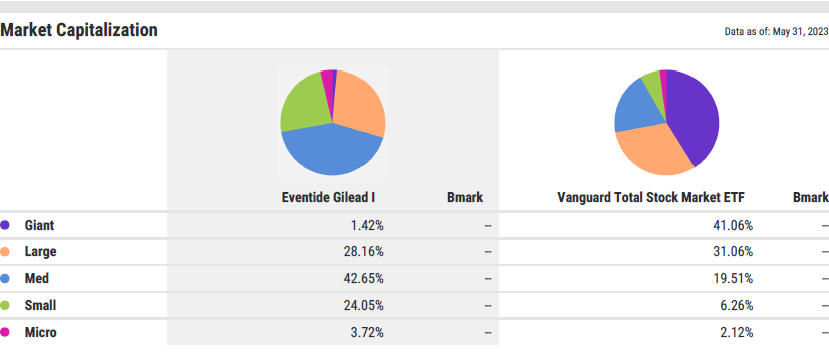

This becomes evident when reviewing the objectives and underlying holdings of each fund analyzed.

There is great variation of security selection within the funds, even when there are similar stated objectives.

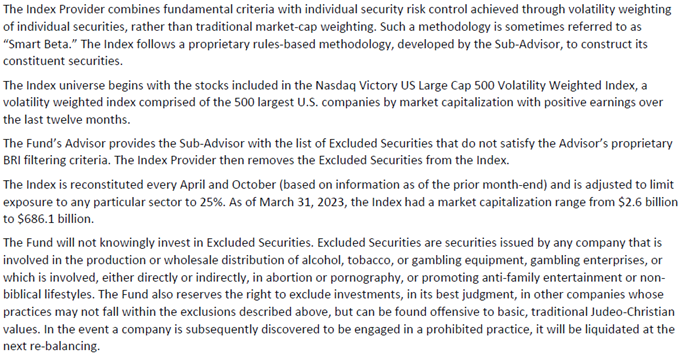

Determining how much “sin” is too much varies widely across funds.

Some funds have a very narrow set of selection criteria and some more broad.

Even funds with the strictest screening criteria fall short, though, when their holdings are examined against the fund’s stated objectives.

All of these factors, I believe, highlight the fundamental problem of faith-based investing funds: This values-based decision is a matter of personal conscience (Romans 14).

And because this values-based decision is unique to each investor, investors who have this conviction are better suited using a direct indexing solution or by utilizing a brokerage window.

These options allow investors to tailor their portfolio to their exact values-based criteria.

However, keep in mind personal screening of securities is also a form of active management.

And investors who do take this approach of selecting and/or excluding individual securities should anticipate reduced long-term performance when compared to a passive market-cap weighted index fund.

In full disclosure, I have no money invested in any fund categorized as BRI and do not use direct indexing or brokerage windows.

Pingback: Three Fundamental Flaws of Faith Based Investing Funds - Church Fiduciary

Pingback: A Guide to Church Retirement Plans - Church Fiduciary

Pingback: Five Principles to Become a Successful Investor - Church Fiduciary

Pingback: Pastors: 3 Paradigm-Shifting Investment Facts - Church Fiduciary